Posted on in Blog by Georgia Rei

There are plus's and minus's to paying off your home quickly.

Advanced Systems Homes knows that taking out a home mortgage is not a quick and easy decision. One of the major things to think about is how long should the financing period be?

Many borrowers may be attracted to 15-year mortgages, which have a shorter term and lower interest rates than 30-year mortgages. But such a mortgage may not be right for your needs.

Despite the rise in popularity of the 15-year mortgage, it is not necessarily for everyone. For borrowers, it is important to get as much information about the different common mortgages institutions offer — and to understand the different terms. While the amount being borrowed, or principal of the loan, is often clear, the cost of the loan, or interest rate, is often less so.

In an interview with 24/7 Wall St., Guy Cecala, publisher of Inside Mortgage Finance, said borrowing to buy a home is a more complicated decision than refinancing. It is "much more of a calculation about what you can afford, how secure you are about your job, what's the likelihood you're going to want to move in less than five years."

Borrowers must understand how payments, which consist of principal repayment and interest, will be structured under the different types of mortgages. They need to consider how much they will be paying for the loan, not just now, but in the future as well. And they should also consider their budget, age and other factors before deciding on a mortgage.

These are the questions to ask when deciding between and 15 and 30-year mortgage.

1. Can you afford to pay off the mortgage in 15 years?

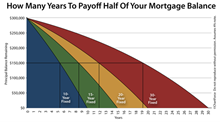

Although a 15-year mortgage offers a lower rate relative to a 30-year mortgage, thereby allowing borrowers to pay interest for only half as long, a 15-year mortgage comes with a higher total monthly payment. This is because the principal must be paid off faster, making each principal payment larger.

Because borrowers pay down the principal balance faster, in the longer run they save on interest payments. Inside Mortgage Finance publisher Guy Cecala noted, "if you can afford the higher payments associated with the shorter-term 15-year mortgage, there is no reason not to take one."

However, because the monthly payments are higher, it can strain borrowers' ability to set aside money for retirement or their kids' college tuition. These borrowers may be better-off with a 30-year mortgage. Similarly, if the higher payments of a 15-year mortgage mean borrowers have less money to invest elsewhere and diversify their portfolios, they may be better off with a 30-year mortgage.

2. Are you buying your first home?

First-time home buyers often benefit from selecting a 30-year mortgage because the monthly payments are lower. A longer-term mortgage can make a more expensive home more affordable for a new buyer. According to Cecala, most first-time home buyers "are trying to get in as much house as they can."

Of course, 15-year and 30-year mortgages are not the only options available to consumers. Borrowers can take an adjustable-rate mortgage, which offers a low initial rate that stays unchanged for some period, such as five years. When the period expires, borrowers could pay more if interest rates rise. But for buyers who are not looking to own their home for too long and who are confident that they will be able to resell the home, an adjustable rate mortgage may be a sensible option.

3. Are you looking to refinance?

If you already have a mortgage and would like to refinance, now may be a good time. Cecala noted that if your current payments on a 30-year mortgage are high enough, you might be able to refinance into a 15-year mortgage and make similar monthly payments while shortening your mortgage term.

An additional factor that may make refinancing more attractive is the current difference, or spread, between interest rates on 15-year and 30-year mortgages. According to Cecala, "historically, the difference between the 30-year fixed rate and the 15-year fixed rate has been about 25 basis points," or about 0.25%. Currently, the spread between the two rates is especially large, at close to 1% in some cases.

4. Are you planning on retiring soon?

How close a borrower is to retiring plays a major role in whether to take out a 15-year mortgage. Typically, borrowers who take 15-year mortgages are at least 40 years old, according to Cecala. These borrowers are often willing to pay off the balance on their mortgages faster in order to retire with little or no outstanding debt on their homes. However, many older homeowners also must weigh prepayment — making early payments on their mortgage — against the need to save for retirement. According to the CFPB, 30% of homeowners aged 70 and older have outstanding mortgages.

5. Do you have a strict savings plan?

Choosing a 15-year mortgage over a 30-year mortgage also may be a worthwhile choice if you are not a disciplined saver. But many people may lack the discipline needed to save long-term, Cecala noted, especially in amounts that would offset what they would save by switching to a 15-year mortgage. He also added that "a lot of times people need that extra money for something else," and so they choose to keep their money in a 30-year mortgage with lower individual monthly payments.

Some truly disciplined savers may actually benefit from carrying their mortgages into retirement. According to a story published by Time magazine: "if you expect to earn more after tax on your investments than you pay after tax on your mortgage, keep the mortgage." What you want to avoid in retirement, however, is a situation where you are juggling a mortgage on top of your basic costs of living, taxes and health care payments.

Still not sure what works for you? Contact one of the ASH experts to help you decide what is right for your family.

Comments

Add Your Own Comment